Q1-26 reporting season begins

As reporting season approaches, the portfolio faces its next round of tests

This update is mainly dedicated to the upcoming reporting season. And excuse the temporary silence. In proper Nordic fashion, the past week was spent on the ski slopes.

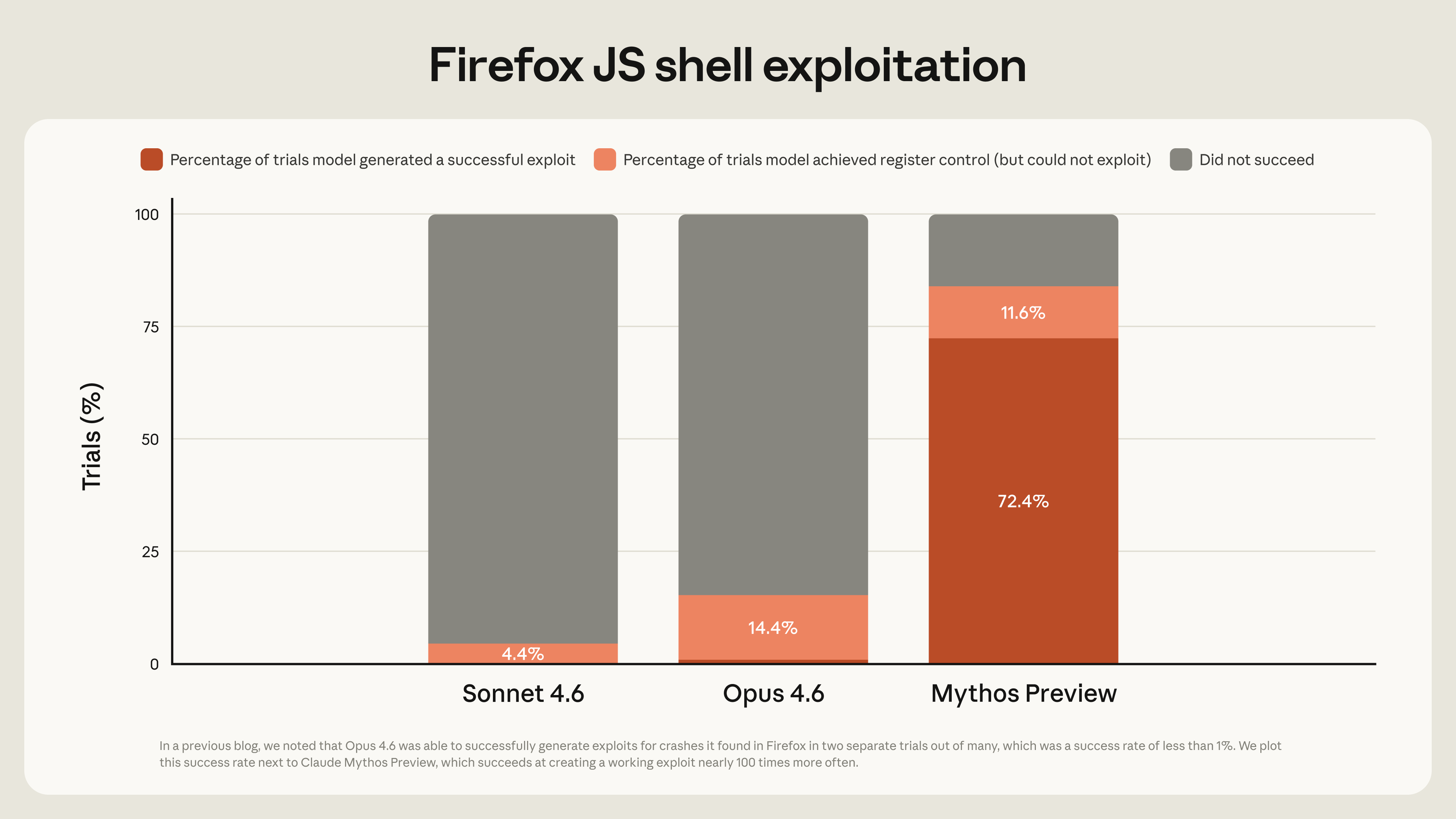

Before getting to the reporting season, one development in the broader news flow really caught my attention. Anthropic released a preview of its newest LLM (“GenAI model”), Mythos, and it has reportedly been deemed too capable for public release. Among other things, it was able to identify new ways to exploit software, including critical systems such as Linux. In response, a project called Glasswing has been formed together with major industry players to help secure some of the world’s most critical software.

And this is still only the beginning. With GenAI, we are likely looking at one of the largest productivity leaps in a very long time. In my view, it may ultimately rank alongside industrialization and electrification. We will, in effect, outsource a large share of intellectual work to machines. That brings enormous opportunity, but also major disruption. It will be fascinating (and at times unsettling) to watch - and should provide us with plenty of investment opportunities. More on that later.

With that said, and back to basics, holdings in Fjord Alpha have been a mixed bag in Q1, both in terms of share price performance and near-term market sentiment. Some names have developed very well and are beginning to see stronger recognition from the market, while others have been more uneven, either due to softer operational momentum, tougher comparisons, or simply a less supportive backdrop.

Among the stronger performers, Ørsted, Hexatronic, Ovzon, and Pexip have stood out. In different ways, they have shown that when fundamentals begin to improve or market confidence returns, the upside can be meaningful.

The more mixed group includes Carasent, Evolution, Vitec, and Embracer. That said, “mixed” does not mean broken. In these cases, the underlying long-term case remains intact, even if the path has been less linear than one would have hoped.

GN Store Nord as you know sold after the divestment of the Hearing division.

Let’s have a look at where the main holdings of Fjord Alpha stand at the moment.

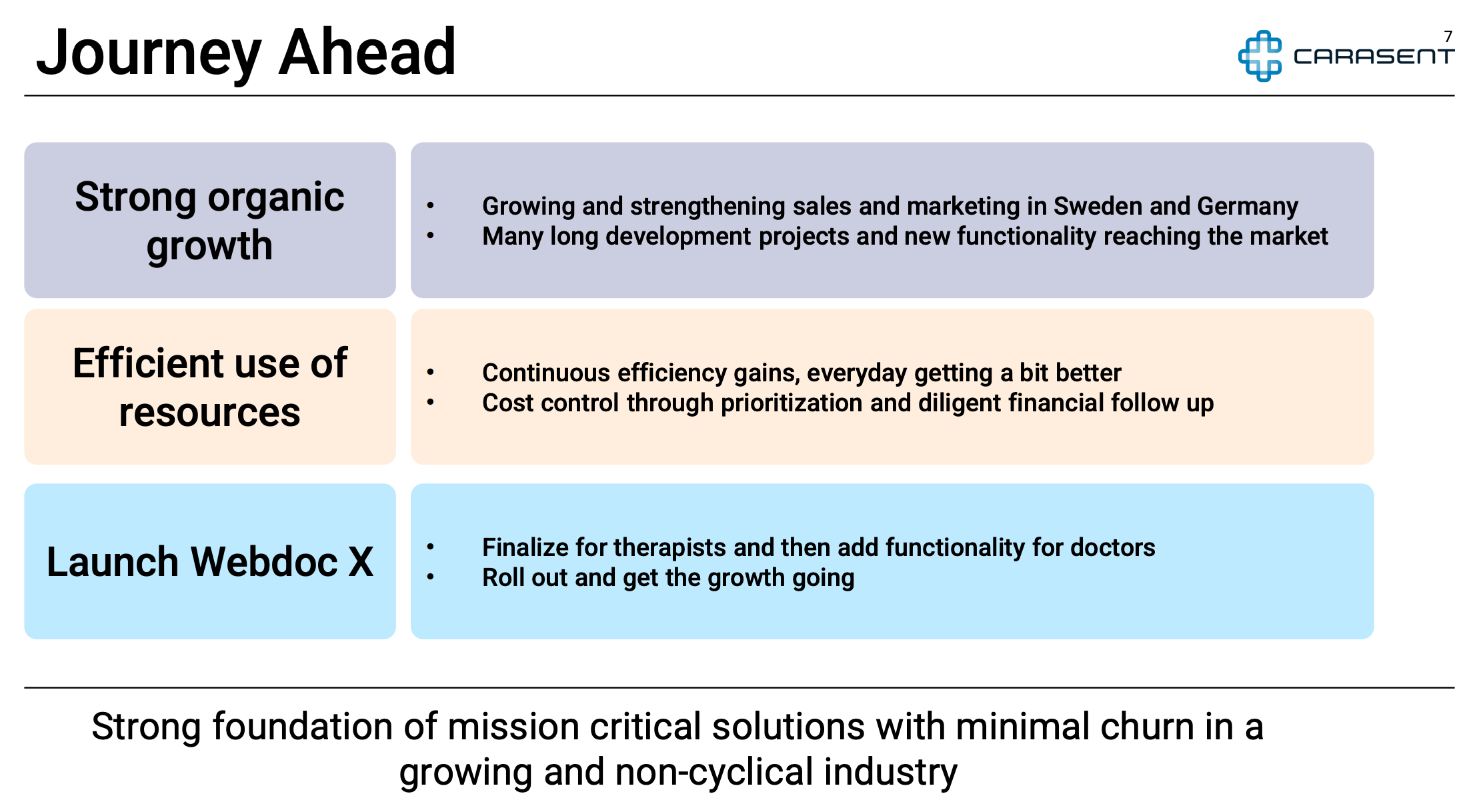

Carasent (Reporting on Apr, 14)

This remains a darling of mine. The company combines deep moats with a long runway for growth across several vectors, while high operating leverage should support meaningful margin expansion over time. There has been virtually no news flow in the last quarter, and the share price has largely been dragged down by the broader SaaS sell-off, albeit with a modest recovery lately. At this valuation, Carasent very clearly passes my 20+% CAGR bar.

The upcoming report should be particularly interesting in terms of the surgery module, the German expansion, and margin development.

Evolution (Apr, 22)

If Carasent news feed has been crickets the last quarter, Evolution is the opposite, making headlines pretty much every week.

To me, the big question is if the negative trend has finally been broken. I am starting to see early signs that the bottom may be in. Analyst sentiment has turned more constructive, activity trackers point to an increasing number of bets, and the recent capital allocation (no dividend, only buybacks) at least is a clear sign of confidence from the Board of Directors. The 200-day moving average has also turned upward for the first time in many months.

As always, this is one to watch closely. I find basically all data points to be of interest. Will we see recovery in Asia and Europe? Do we see continued strong momentum in the US? How are margins developing?

Ovzon (Apr, 23)

There has been limited news during the quarter beyond a small additional order, but the real story here remains the long-term one. The underlying macro tailwinds have probably never been stronger. Defense spending across Europe is rising sharply, and the willingness to reduce strategic dependence on the US appears to be increasing as well. In that context, Ovzon looks very well positioned. This is a long-term play, and I will be watching carefully for any larger updates.

Vitec Software (Apr, 23)

The stock has been heavily de-rated, as you know, but it has held up relatively well in the SEK 220–250 range since early February and has withstood the broader market turbulence better than one might have expected. My sense is that the market’s SaaS-related concerns around Vitec have become overdone.

Two solid acquisitions (Autonet and Infometric) during the quarter will provide growth tailwind. These two deals alone add nearly SEK 190 million in inorganic revenue to 2026 estimates before the year has effectively started, securing ~5% inorganic growth.

Analyst sentiment also remains clearly supportive, with all covering analysts currently at BUY.

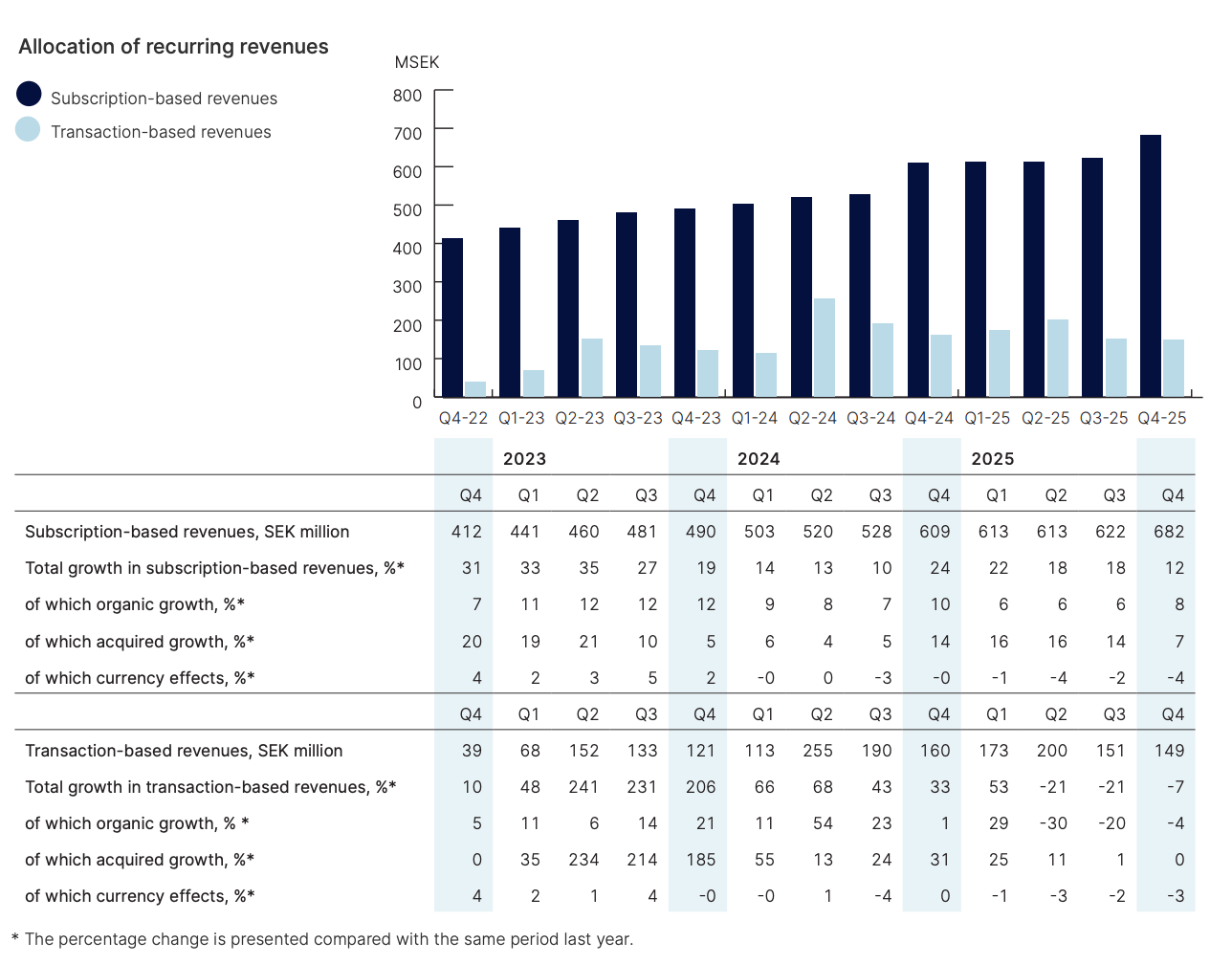

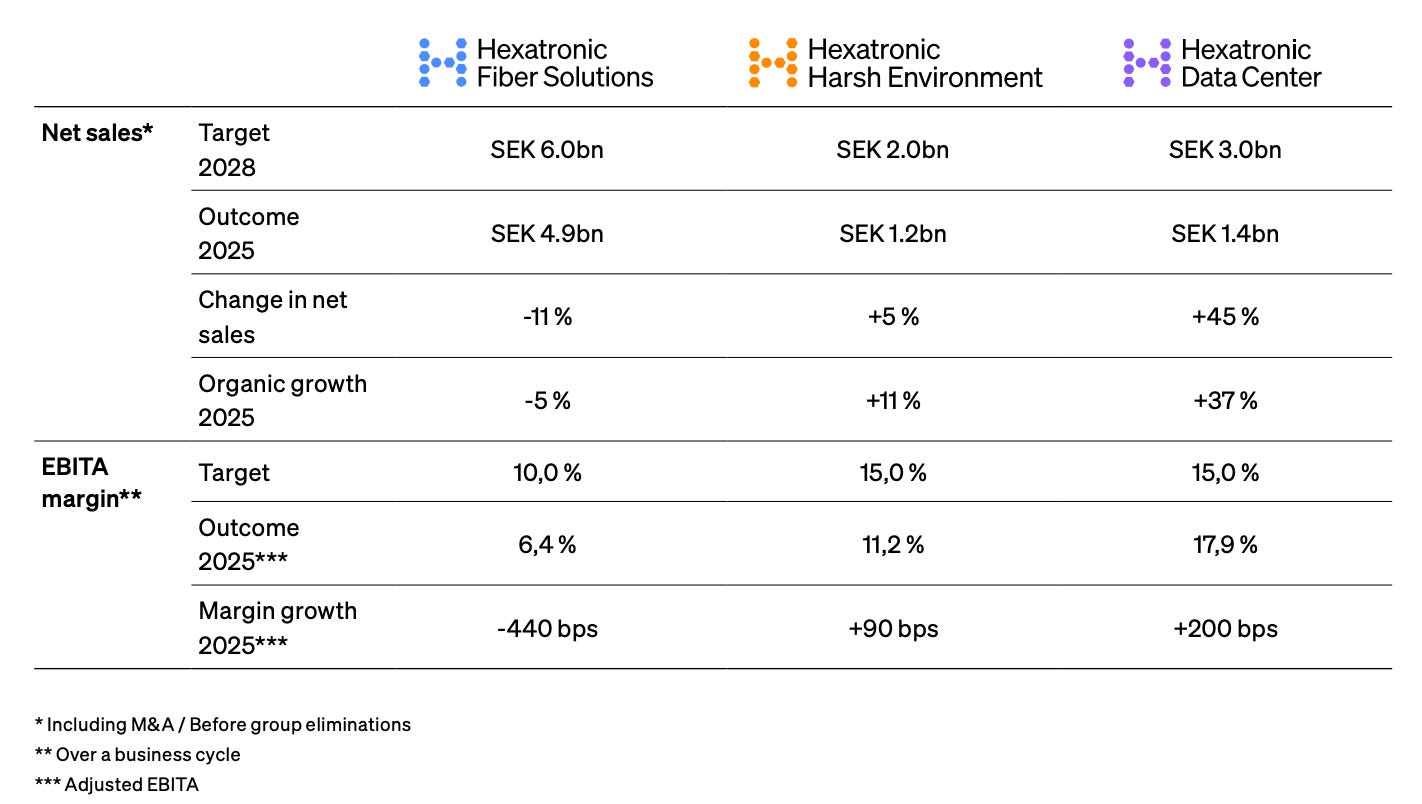

Hexatronic (Apr, 29)

Hexatronic has had a very strong start to the year, with the stock up more than 50% year to date. The macro backdrop also remains supportive, particularly through exposure to data centers and a meaningful US footprint. News flow has been limited in Q1, beyond an acquisition out of Germany. The 2028 targets are aggressive (see below), and will be interesting to see how we are tracking in Q1.

RaySearch (Apr, 29)

For this one I refer to my very recent write-up.

Pexip (May, 5)

Pexip has remained comparatively stable and is up from our original entry. The broader case is still the same. It is a well-positioned business with attractive exposure to secure and mission-critical communication solutions. It may not be the most talked-about name in the portfolio, but it continues to look like a solid long-term holding with room for both operational progress and multiple expansion.

There has been no major updates from the company during the Q1, and I will mainly be looking for signs that my thesis is still holding.

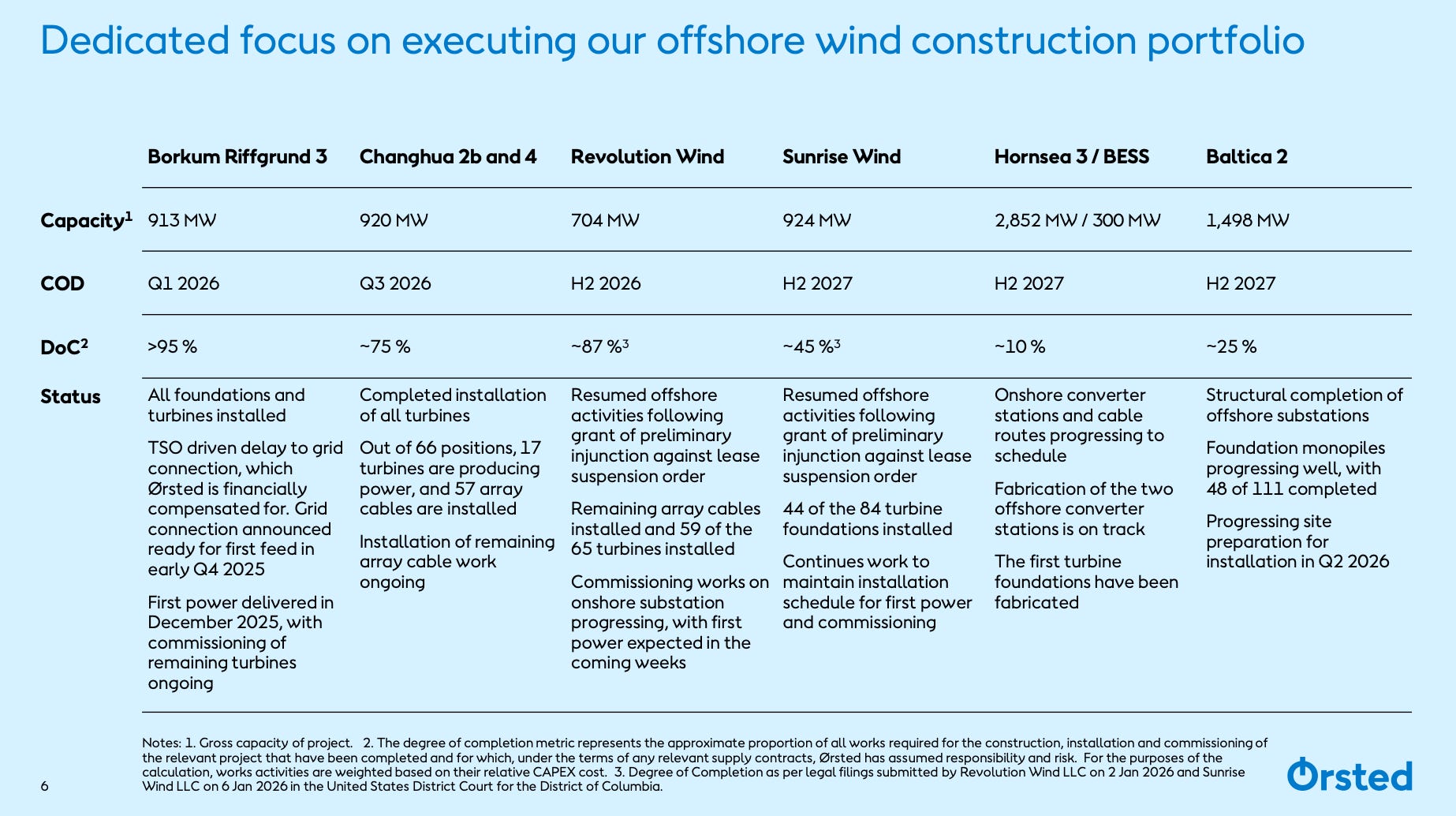

Ørsted (May, 6)

Speaking of macro trends, Ørsted also looks very well positioned. Renewable energy remains a highly attractive theme, particularly in an environment of elevated energy prices, and the company has also taken steps to reduce its US exposure. The stock has rerated sharply and is up 34% year to date, but the broader strategic case still remains compelling.

Embracer (May, 20)

Embracer remains a more controversial name, but that is also what makes it interesting. Sentiment is still burdened by the company’s history, and confidence will need to be rebuilt over time. That said, the underlying asset base is substantial, and there is clear potential for value creation if management continues to improve execution, simplify the structure, and demonstrate greater capital discipline. This is not the cleanest story in the portfolio, but the upside is significant if the company gets it right.

The major update from Q1 is of course the announcement of the new Lord of the Rings movie, a clear sign of monetization of Embracer’s deep IP portfolio - and a movie I personally will be looking forward to!

In summary

So while the portfolio has been partly a mixed bag in the short term, the underlying businesses are performing well. Reporting season will no doubt bring both encouragement and frustration, but that is also what makes investing interesting.

In the end, the real test is not quarter-to-quarter perfection and near-term stock price development, but whether the underlying businesses continue to strengthen over time.

Reporting season, game on!