RaySearch AB: From planning tool to oncology software platform

RaySearch is evolving beyond treatment planning into a broader, workflow-critical software platform. If that continues, the upside should come from both earnings growth and re-rating.

1. Introduction

RaySearch is a Swedish oncology software company best known for treatment planning in radiation therapy. The stock has fallen sharply from prior highs, despite the business today appearing more profitable, more recurring, and more strategically relevant than the market seems to credit. That combination makes the stock interesting for Fjord Alpha.

The company is still primarily perceived as a treatment planning software vendor. That is true, but increasingly not fully correct. As radiation oncology becomes more data-intensive and operationally complex, software is becoming more central to clinical value creation across planning, workflow, treatment execution, and analytics.

This matters because the industry’s economic center of gravity is shifting. Historically, value accrued mainly to the treatment machine (hardware), with software playing a supporting role. Today, precision, interoperability, workflow integration, and efficiency increasingly increase the strategic importance of the software layer.

The key question is therefore not only whether RaySearch has a strong position in treatment planning. It is whether the company is evolving into a broader, workflow-critical oncology software platform that the market still values through a narrower lens. If that transition continues, the upside should come from both earnings growth and multiple expansion.

Let’s dig into it.

2. Background: From academics to clinical infrastructure

Origins: Mathematics as the original USP

RaySearch was founded in 2000 by Johan Löf, whose work at Karolinska centered on optimization algorithms for radiation therapy. The founding proposition was simple, i.e. better mathematics produce better treatment plans.

For its first decade, the company licensed algorithms to larger players like Philips, Nucletron, IBA, thereby generating royalty income while embedding its IP deep into the industry’s infrastructure. That OEM phase built a reputation for scientific excellence and gave management time to deepen the technical moat before going direct.

It also revealed the limitations of being a component supplier to slow-moving hardware vendors.

RayStation: Moving from supplier to platform owner

The launch of RayStation in 2009 was the decisive pivot. Instead of licensing algorithms into third-party systems, RaySearch chose to own the full treatment planning experience such as interface, optimization engine, workflow, and customer relationship.

The timing was excellent. Rising clinical complexity, the expansion of proton therapy, and the emergence of VMAT all favored a modern planning platform. RayStation won first in the hardest environments - proton centers and elite academic hospitals, and then leveraged that credibility across the broader market. If the software handles the most complex particle therapy cases, it can obviously handle conventional photon work. That top-down reputation became a powerful commercial asset.

The ecosystem phase: Beyond planning

The next phase came from a simple insight, that a great treatment plan is useless if the rest of the workflow such as scheduling, documentation, treatment control, analytics, runs on disconnected legacy systems.

That realization drove RaySearch into adjacent categories. RayCare for oncology information, RayCommand for treatment control, RayIntelligence for analytics. This was a move up the value chain, from departmental tool to operational infrastructure. A treatment planning system lives inside the physics team. An OIS and treatment control layer sit at the operational core of the clinic.

That distinction is the equity story.

3. Technical engine: Performance as a source of competitive advantage

In radiation oncology, software differentiation is not just a matter of interface or workflow. At the highest level, it depends on computational performance, physics accuracy, and the ability to function reliably across increasingly complex clinical settings. RaySearch’s technical position appears to rest on four reinforcing advantages: speed, openness, credibility in demanding treatment environments, and workflow-embedded automation.

Computational performance

Treatment planning is computationally intensive, and that burden rises with clinical complexity. RaySearch has invested heavily in high-performance calculation and optimization, including GPU-based capabilities, which is especially relevant in advanced use cases where accurate dose calculation can otherwise become a practical bottleneck. Faster planning enables more iteration, broader scenario testing, and better use of limited clinical time. Over time, that can become a source of stickiness, as clinics build workflows around a planning environment they are reluctant to slow down.

Vendor neutrality

A second differentiator is openness. Much of radiotherapy remains structured around vertically integrated vendor ecosystems, but many providers operate mixed machine environments and value flexibility at the software layer. RaySearch’s vendor-neutral positioning allows clinics to standardize planning and workflow across heterogeneous hardware fleets without having to replace installed equipment. In that setting, the software layer can become more embedded in day-to-day clinical operations than any individual machine, which strengthens customer retention and strategic relevance.

Proton therapy as a proof point

RaySearch’s position in proton therapy also matters beyond the revenue contribution itself. Proton planning is among the most technically demanding areas in radiation oncology and requires high levels of computational sophistication, accuracy, and clinical reliability. Success in that segment therefore serves as an external proof point of technical quality. Credibility earned in proton centers can support broader adoption in conventional photon therapy, where buyers may view performance in the most demanding settings as evidence of broader robustness.

Workflow-embedded automation

Automation is most valuable when it reduces friction inside systems clinicians already use every day. RaySearch appears well positioned here by embedding automation directly into planning workflows rather than treating it as a separate capability. In practice, that can reduce manual steps, improve consistency, and ease workflow pressure in resource-constrained departments. Commercially, this matters because customers often value time savings and usability more clearly than abstract innovation.

Taken together, these capabilities support the view that RaySearch’s technical position is not merely product-level differentiation, but part of a broader platform advantage.

4. Product ecosystem: Replacing the brain

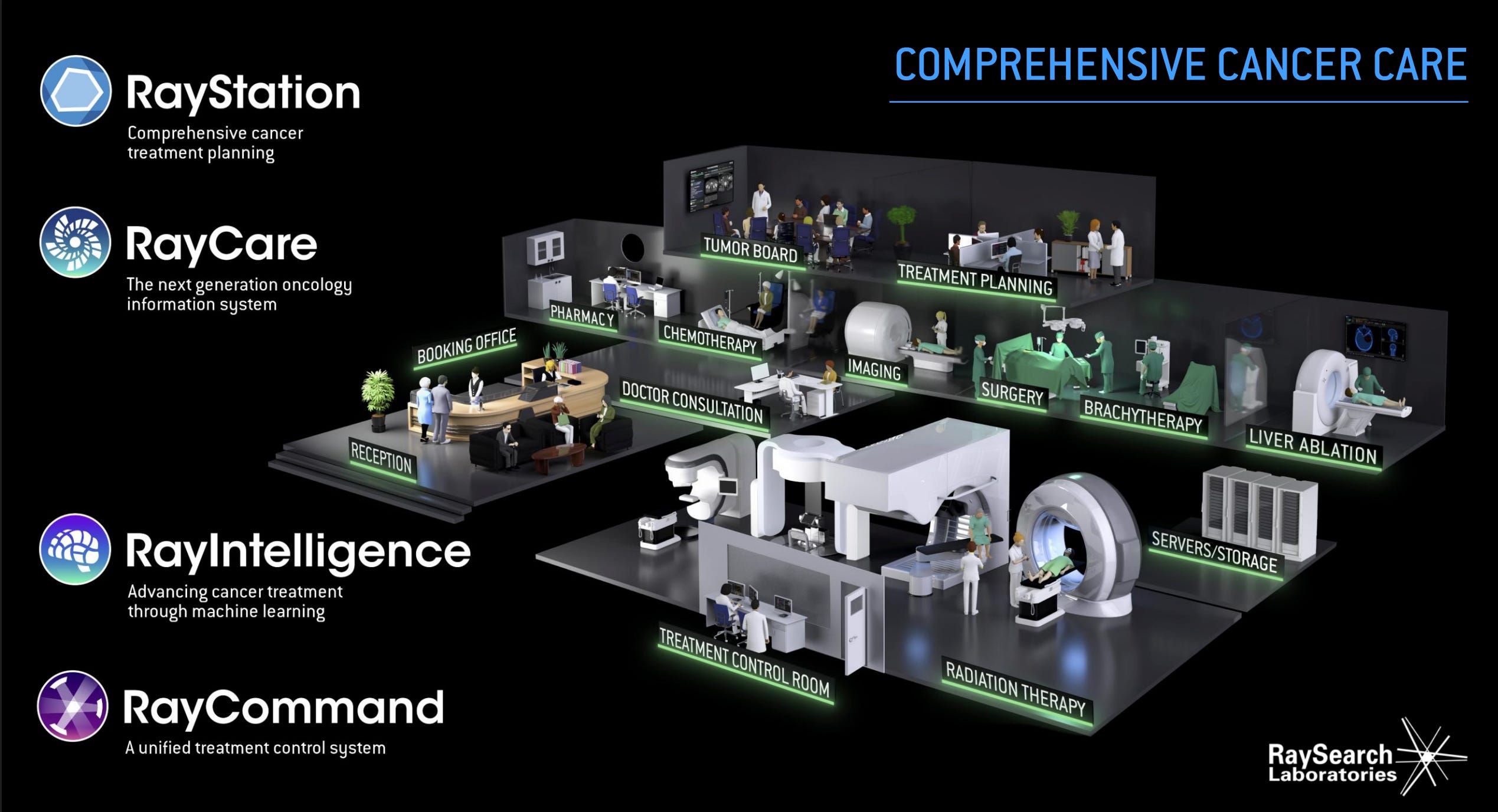

RaySearch’s strategic logic is to leave the machine in place, replace everything above it. Decouple the clinic’s intelligence layer from the incumbent hardware stack. There are four key products in the ecosystem; RayStation, RayCare, RayCommand and RayIntelligence.

RayStation: The beachhead

RayStation is the entry point. It solves an immediate, visible problem which is faster, higher-quality treatment planning, and once installed, it embeds RaySearch into departmental routines, training, and clinical habit. Switching costs are high. That makes RayStation both a strong standalone product and an effective commercial wedge for the broader platform.

RayCare: The commercial unlock

RayCare is the most strategically important product in the portfolio. It moves RaySearch from planning into operational infrastructure such as workflow orchestration, not just record-keeping and billing.

The commercial bottleneck was always interoperability with Varian TrueBeam systems. That barrier constrained adoption in the largest installed machine base. The progress made in 2024 and 2025 changes the math. A clinic can now upgrade its software layer without replacing its hardware. That is the single most important commercial development in this story.

RayCommand: Optionality on fragmented hardware

RayCommand extends RaySearch into treatment control and creates asymmetric optionality. Large incumbents build their own control systems, but smaller or newer machine vendors often lack the resources for a full software stack. If hardware fragmentation increases, RaySearch benefits as the default software layer for new entrants. The company profits from hardware disruption rather than being threatened by it.

RayIntelligence: Building the data layer

RayIntelligence converts installed software presence into “data advantage”, aggregating operational and treatment data to benchmark workflows and lay groundwork for future clinical algorithms. Companies that control planning and workflow data will be best positioned to train and deploy the next generation of clinical AI. RaySearch is quietly building toward that position.

5. Market structure and industry tailwinds

Several industry shifts appear to be increasing the strategic value of software relative to hardware in radiation oncology. In each case, the common pattern is the same: as treatment becomes more precise, more adaptive, and more operationally demanding, the software layer becomes more important to clinical performance and workflow efficiency.