Vitec Software Group Q1-26: Steady hands, expanding margins, and the AI advantage

I take a closer look at how margin recovery, disciplined execution, and selective M&A are reinforcing the Vitec investment case following the Q1-2026 report release.

I’ve taken a look at Vitec Software Group’s Q1 2026 report. If there was any remaining investor concern following a slight margin dip at the end of 2025, this first-quarter report offers a comeback. CEO Olle Backman put it well on the earnings call - the company is firmly back on track to delivering the gradual profit margin improvements that have long been the hallmark of its financial targets.

As per recent quarters, and despite global uncertainties making the private M&A market somewhat hesitant, Vitec’s operational engine is humming along smoothly. The company’s niche / vertical focus provides a defensive moat that is more resilient to market disruptions.

The margin story: Discipline pays off

The standout narrative of Q1 is undoubtedly the return to margin expansion, with profitability outpacing top-line growth.

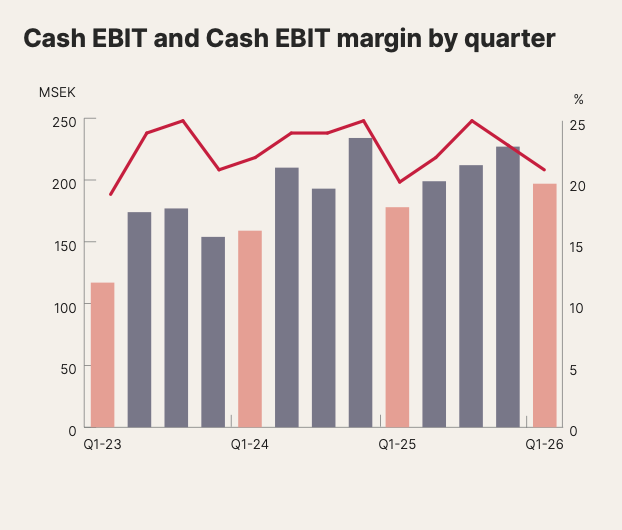

EBITA increased by 11% to SEK 244 million, lifting the margin to 26%.

Similarly, Cash EBIT, the crucial internal metric for Vitec, grew by 11% to SEK 197 million, yielding a 21% margin.

This wasn’t just a happy accident. Management highlighted that these margin expansions are the direct result of higher revenues paired with 1) strict cost control and 2) early efficiency gains. Vitec has managed to drive this growth without actively adding to its organic headcount during the quarter, signaling that their internal productivity initiatives are bearing fruit.

Revenue drivers: Healthy subscriptions and an Enova boost

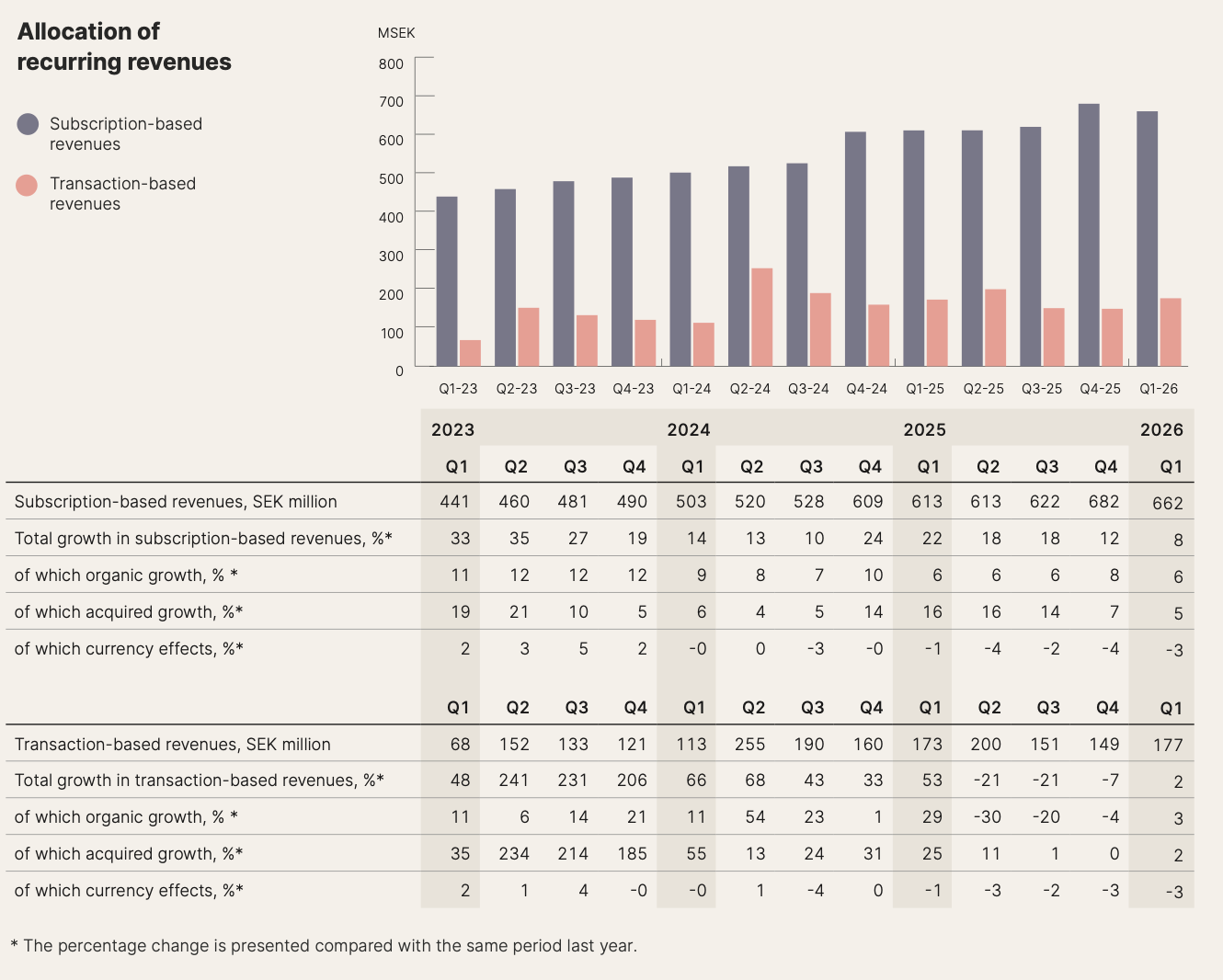

Digging into the top line reveals a healthy mix. Total recurring revenues grew to SEK 839 million (subscription + transaction), making up a high 88% of total net sales.

The core subscription-based revenue grew by 8% overall, with organic growth coming in at a solid 6%. I see this organic growth is structurally sound, driven evenly by a 50/50 split between price adjustments and actual volume increases via upsells and innovation.

Transaction-based revenues, which tend to be volatile, provided a pleasant surprise by beating analyst forecasts by 20% to reach SEK 177 million. This was largely driven by Enova, Vitec’s Dutch energy balancing subsidiary. Geopolitical tensions in the Middle East caused a spike in Dutch gas prices during March, which in turn elevated balancing service activity and boosted Vitec’s transaction line. While management was quick to remind analysts that this segment remains weather- and market-dependent, it certainly provided a nice tailwind for the quarter.

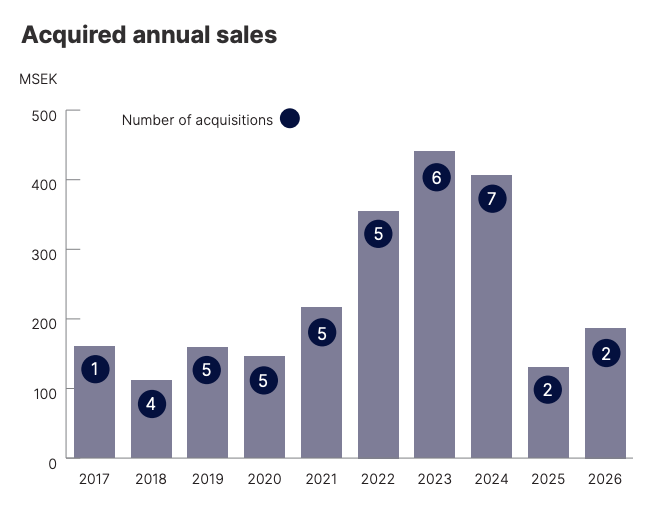

M&A: Navigating a hesitant market

As I have written about earlier, Vitec’s identity as a serial acquirer was reinforced early in the year. The company welcomed over 75 new colleagues through two high-quality acquisitions:

Autonet B.V.: A Dutch software provider for the vehicle dismantling industry.

Infometric AB: A Swedish company focused on energy and water consumption analytics for property management.

Olle mentioned that the business environment feels cautious, with potential sellers showing reduced investment appetite and hesitation. Rather than overpaying to force growth, Vitec has cautiously lowered its own price expectations and is maintaining an active dialogue pipeline, waiting for sellers’ expectations to align with reality.

The AI perspective: Why “legacy” is a strength

Perhaps the most interesting comments in the Q1 earnings call revolved around AI. In a market where it’s easy to fear that agile AI startups will disrupt legacy software providers, Backman flipped the narrative.

He argued that having legacy code is a massive advantage because “legacy is what brought us here” and “legacy is what our customers are paying for right now”. In the world of mission-critical vertical software, there is no tolerance for failure, and the software just has to work.

Instead of being a threat, AI is serving as a tool for Vitec. Modernizing older code has suddenly become much faster and cheaper thanks to AI-assisted development. Furthermore, while I see Vitec rapidly adopting these tools internally to speed up ticket resolution and bug fixing, their customers are moving much slower. Clients prefer a “wait-and-see” approach and proof of value before fully committing to AI features. This cautious customer base virtually eliminates the risk of sudden, AI-driven churn.

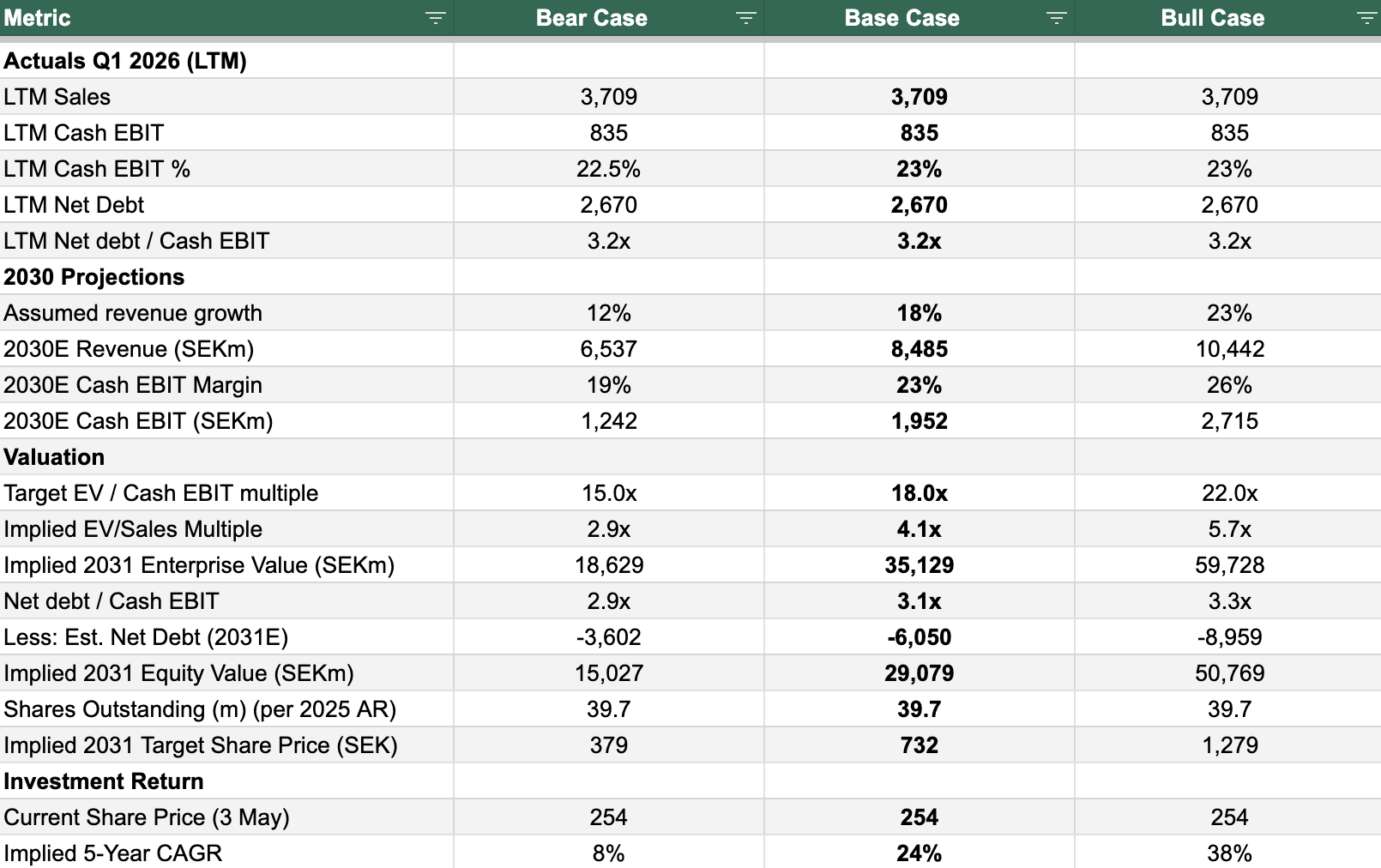

Valuation and bottom line

My valuation model still supports a BUY, handsomely beating my 20+% expected CAGR hurdle rate over the next five years. For a deep dive into the underlying valuation assumptions, please see the extensive valuation section in my last report update.

To wrap up, Vitec closed out the first quarter of 2026 looking stable. With a fresh, oversubscribed SEK 700 million bond issued to secure capital, a strong cash conversion rate of 80%, and no planned organic headcount increases, the company is well positioned. They have the financial firepower to execute acquisitions when the private market opens up further, and the operational discipline to keep squeezing higher margins out of their existing portfolio.

Taken together, the Q1 report reinforces my constructive view on the stock. The core investment case remains intact, and with margins moving in the right direction again, I continue to view Vitec as highly attractive on a medium- to long-term basis.

Given the extreme pessimism currently surrounding the SaaS sector (driven by “vibe coding” and AI disruption fears), I am not going “all in” at once. I view this as a gradual accumulation zone, I am buying now, but keeping some powder dry until technical trends (MA50 and MA200) confirm the bottom is truly past us.