Pexip Q1-26: Strong growth and margins - but not cheap

Re-accelerated ARR growth, record profitability, and a stronger segment mix make the Bull Case more credible. But valuation is no longer on our side.

Pexip’s Q1-26 was the kind of quarter that changes the probability weighting of an investment case. See my original longer write-up on Pexip here.

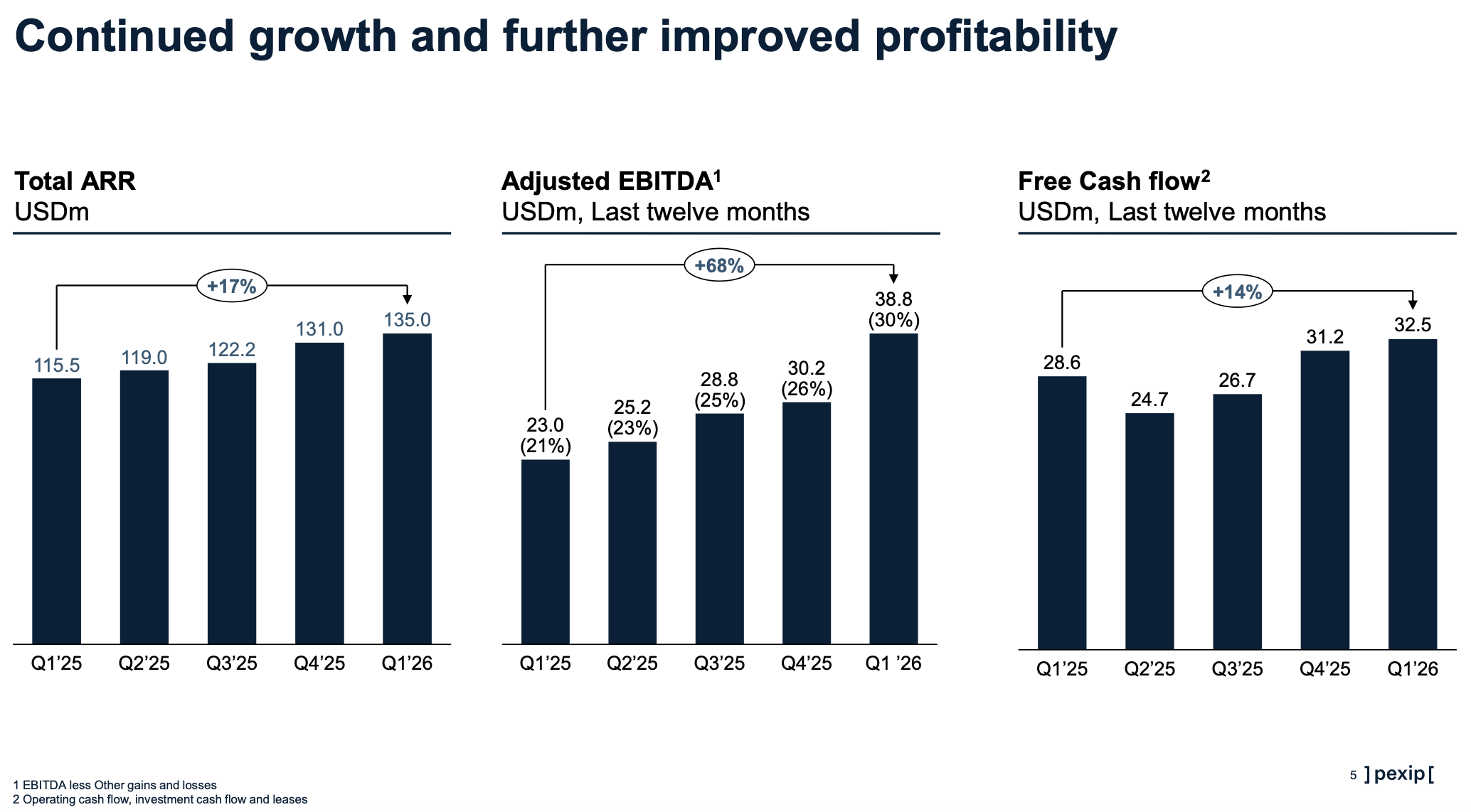

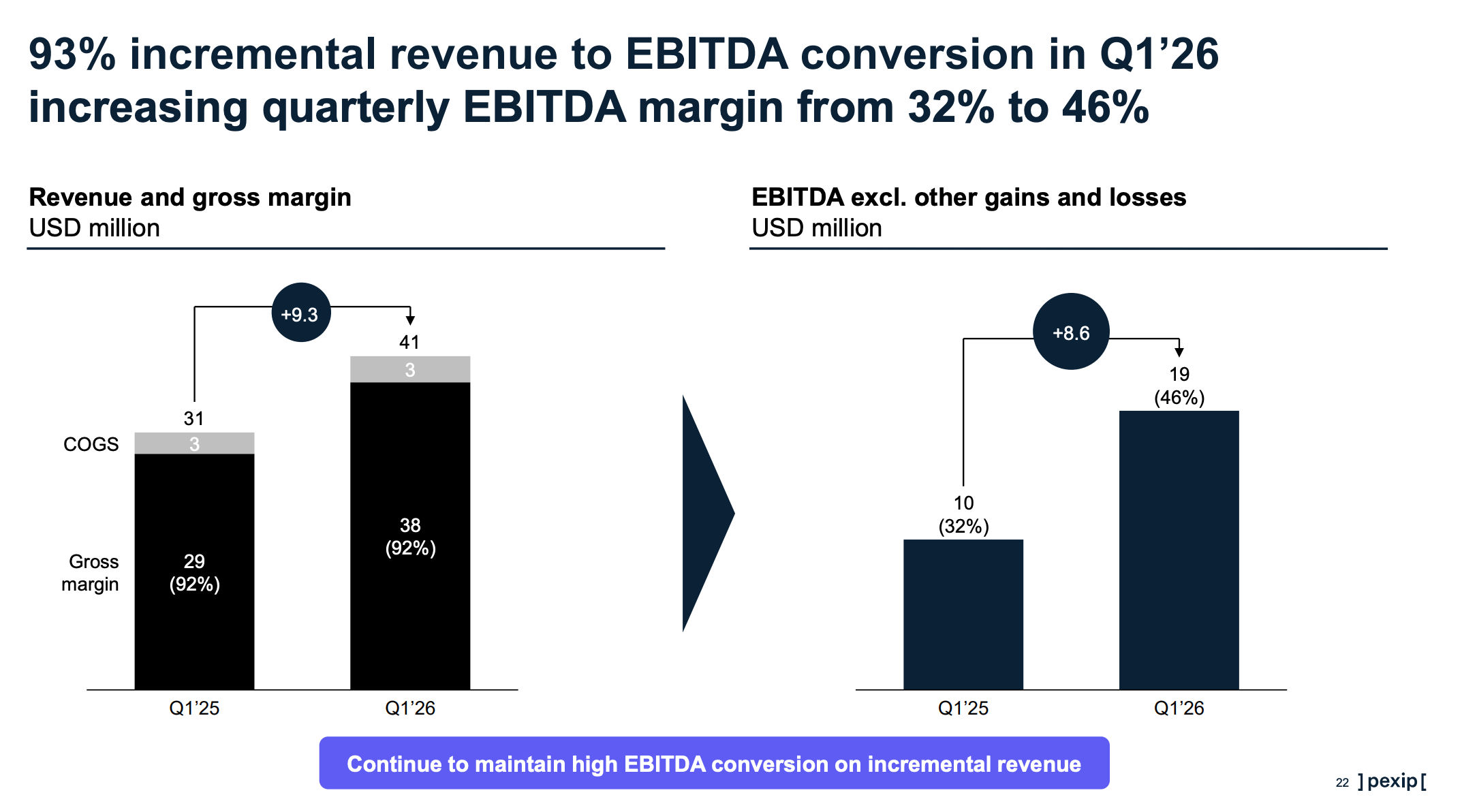

ARR growth re-accelerated to 17% year over year, reaching $135.0 million, up from 12% in the prior period. At the same time, profitability stepped up meaningfully, with a record 46% Adjusted EBITDA margin in the quarter. Even allowing for some timing effects, the 93% conversion of incremental revenue into EBITDA shows that Pexip is becoming a much more scalable business.

On an LTM basis, the company now screens firmly as a Rule of 40 performer, combining 17% ARR growth with a 30% EBITDA margin for a score of 47.

The old Base Case now looks too cautious. Secure & Custom Spaces is becoming a larger part of the mix, blended growth is moving toward the high teens, and Connected Spaces is contributing rather than dragging down the group. The Bull Case is therefore more credible than it was before Q1.

The problem is that the market has noticed. With the share price now hovering just above NOK 80, the easy re-rating is probably behind us. Pexip is clearly a better business than it was a few quarters ago, but at today’s valuation, execution now needs to keep catching up with the stock.

The changing business mix

Pexip enters the next phase of growth with clear momentum, but also with a business mix that is becoming less linear from quarter to quarter. Management’s Q2 2026 ARR guidance of $137–$141 million points to continued growth, while also reflecting the reality that a larger share of the pipeline now comes from bigger, more complex enterprise and public-sector deals. These opportunities can be highly attractive, but the exact timing of when they close may shift across quarter boundaries.

The broader strategic backdrop remains supportive. Demand for secure, sovereign collaboration solutions continues to strengthen, particularly in Europe, where technology sovereignty is moving from an ambition to a more concrete procurement requirement. This creates a favorable environment for Pexip’s Secure & Custom Spaces business, while the more mature Connected Spaces segment continues to provide stability, cash generation, and a practical bridge for enterprises modernizing their meeting-room infrastructure.

Against this backdrop, the investment case is increasingly built around two complementary engines. Secure & Custom Spaces as the higher-growth, higher-leverage segment, and Connected Spaces as the resilient cash-generating platform.

Secure & Custom Spaces: Strong growth and more strategic

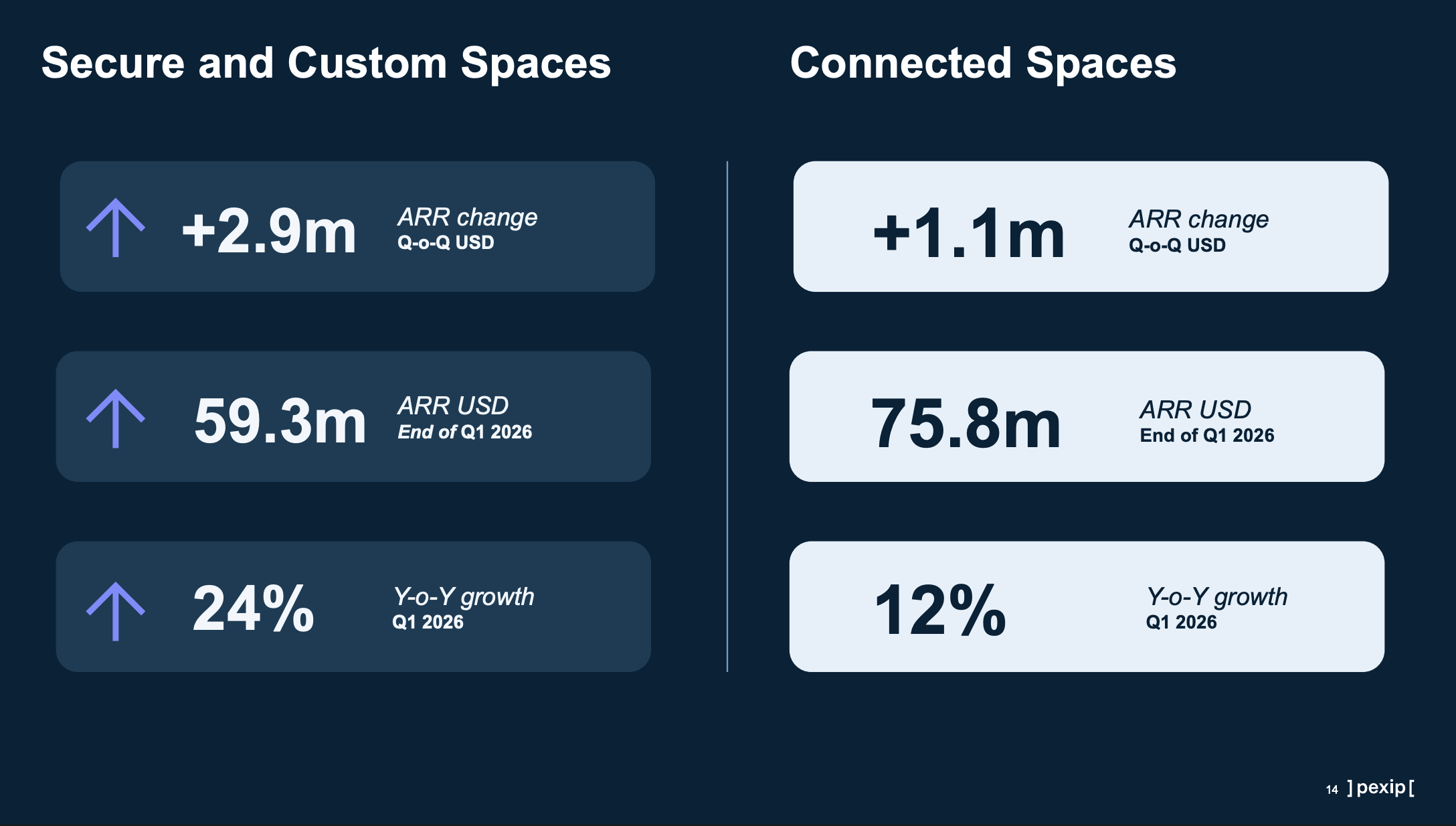

Pexip’s Secure & Custom Spaces segment has moved well beyond its earlier positioning as a defense-led niche. It is now one of the company’s main growth engines, representing 44% of total ARR. In Q1 2026, the segment reached $59.3 million in ARR, up 24% year over year, with $2.9 million of sequential growth. Net Revenue Retention also improved to 104%, its highest level since 2021, supported by both new customer wins and continued expansion within the existing base.

The growth is increasingly broad-based across regulated and high-stakes environments. Q1 included a large three-year contract with a Canadian healthcare provider, while a European Justice System is now using Pexip to support more than 3,000 court cases per day. Defense remains an important anchor, contributing $1.3 million of the quarter’s growth, with both the U.S. Department of Defense and a European Ministry of Defense expanding their secure meeting deployments.

The segment is also becoming more profitable as Private AI adoption grows. Management indicated that customers adopting features such as captions and transcripts can generate a 20–30% revenue uplift. Since customers cover the underlying compute costs, these features appear to carry attractive incremental margins and supported Pexip’s 46% Adjusted EBITDA margin in the quarter. Importantly, this growth was delivered with nearly flat operating expenses, with 93% of incremental revenue converting to EBITDA. This level of operating leverage is pushing Pexip firmly into Rule of 40 territory, with an LTM combined score of 47.

Connected Spaces: Stabilizing and cash generating

Connected Spaces also performed better than expected in Q1. After having been viewed as a more mature, slow-growth part of the business, the segment delivered 12% year-over-year ARR growth, reaching $75.8 million. The $1.1 million sequential increase marks a clear improvement from the flatter performance seen in late 2025. NRR improved to 98%, suggesting that churn has normalized after the more uneven Q4 period.

The main driver is momentum in Native Rooms, Pexip’s interoperability solution for Microsoft Teams, Zoom, and Google Meet rooms. This remains a practical and valuable proposition for large enterprises that want to standardize on modern collaboration platforms without writing off existing room hardware. A key upcoming catalyst is the planned June 2026 rollout of Pexip Connect for Microsoft Teams Rooms on Android. Management sees this as opening up a much larger opportunity, particularly in organizations with mixed device environments, as the Microsoft Teams Rooms installed base continues to expand rapidly.

Financially, Connected Spaces continues to provide high-quality earnings. Despite higher cloud compute usage, gross margins remained stable at 92%, supported by operational efficiencies and cloud platform rebates. This makes the segment an important cash flow contributor, helping Pexip generate $19.8 million of free cash flow in Q1.

Very strong margin development

The margin development in Q1 was arguably the clearest proof point in the quarter. Gross margin remained very strong at 92%, despite higher cloud usage, which confirms that the core software model still has attractive economics.

The bigger shift was below gross profit. Operating expenses were broadly flat year over year, while revenue and ARR continued to grow. That combination created a very strong drop-through to earnings, with Adjusted EBITDA reaching $18.7 million and the quarterly EBITDA margin hitting a record 46%. Even if some of the quarter was helped by timing effects and accrual reversals, the direction is clear. Pexip has become a much more disciplined and scalable business.

What stands out is the 93% conversion of incremental revenue into EBITDA. That is not a normal software margin profile unless the company has strong pricing, limited incremental delivery cost, and a cost base that does not need to grow in line with revenue. Pexip appears to have all three. Private AI can add revenue uplift without Pexip carrying the compute burden, Secure & Custom is becoming a larger part of the mix, and Connected Spaces continues to generate high-quality cash flow.

Future management guidance

Management’s Q2 guidance points to continued growth, with ARR expected to land between $137 million and $141 million. The wider range reflects a pipeline increasingly driven by larger enterprise and public-sector contracts, where the underlying demand is strong but closing dates can move between quarters.

The message is therefore positive, but not perfectly linear. Pexip appears to have good momentum, especially in Secure & Custom, supported by sovereign IT demand and regulated-sector wins. At the same time, investors should expect some lumpiness as larger deals become a bigger part of the mix. If Q2 lands toward the high end of guidance, it would be a strong signal that the Q1 re-acceleration is not just a one-off.

Base, Bull and Bear Case update

Q1-26 does not change the core thesis, but it does change the probabilities. The original setup was built around a two-speed business: Secure & Custom as the growth engine and Connected Spaces as the slower cash cow. That still looks right, but Q1 suggests the growth engine is stronger, the cash cow is healthier, and the margin potential is higher than previously assumed.

Base Case: needs to move up

The original Base Case assumed Pexip would remain a low-teens ARR grower, with Secure & Custom offsetting a flat or slightly declining Connected Spaces business. After Q1, that now looks too cautious.

Blended ARR growth has accelerated to 17%, versus the original 12% Base Case assumption.

Secure & Custom grew 24% year over year and now represents 44% of total ARR.

Connected Spaces grew 12% year over year, rather than being flat.

LTM EBITDA margin is already 30%, above the original Base Case assumption of 25%.

The company is now already inside Rule of 40 territory, with an LTM score of 47.

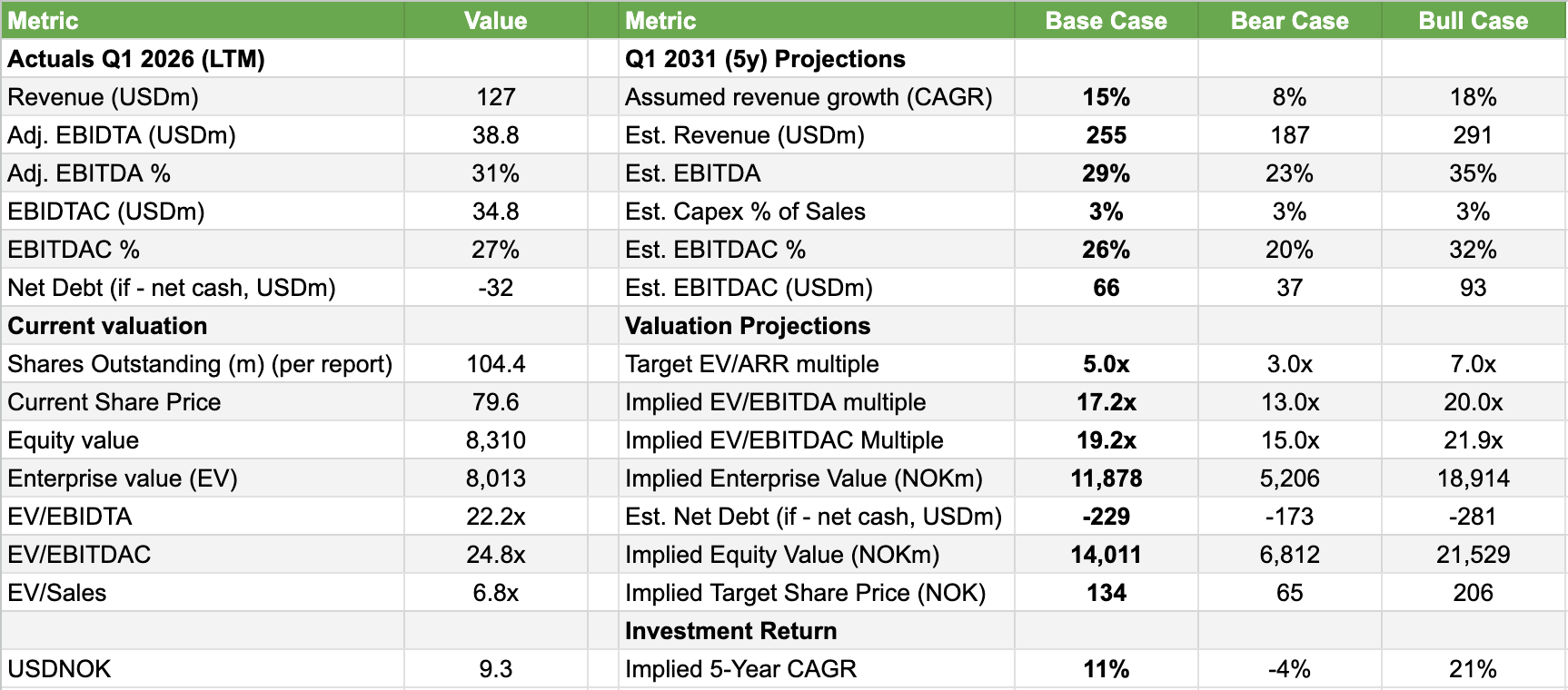

What to assume now: the Base Case should move from “low-teens ARR growth and mid-20s EBITDA margin” to something closer to 14–16% ARR growth and a 28–30% EBITDA margin. This still leaves room for some normalization after a very strong Q1, but it better reflects the current run-rate.

Bull Case: now more credible

The original Bull Case required blended ARR growth moving toward 18%, continued mix shift toward Secure & Custom, and EBITDA margins expanding toward 30%. Q1 delivered much of this earlier than expected.

Blended ARR growth is already close to the original Bull Case level.

Secure & Custom continues to scale and should become an increasingly important part of group growth.

Connected Spaces is not dragging the group down, which makes the blended growth profile more attractive.

Operating leverage is coming through clearly, with 93% of incremental revenue converting into EBITDA in Q1.

The Rule of 40 target has effectively been reached earlier than expected.

What to assume now: the Bull Case should still assume 17–19% ARR growth, but the margin assumption can be more confidently set around 30%+ EBITDA margin. The real upside case is no longer just margin expansion; it is that Pexip can sustain high-teens ARR growth while keeping margins around 30%. That would justify a higher-quality software multiple.

Bear Case: less likely, but still relevant

The original Bear Case was built around Connected Spaces becoming a “melting ice cube” and dragging blended growth below 10%. Q1 weakens that argument, at least for now.

Connected Spaces grew 12% year over year, rather than shrinking.

NRR improved to 98%, suggesting churn has stabilized.

Native Rooms appears to be giving the segment a clearer growth driver.

The segment continues to support group cash flow and profitability.

Secure & Custom is now large enough to have more influence on the group trajectory.

What to assume now: the Bear Case should be softened. Instead of assuming a sharp decline in Connected Spaces, it is more reasonable to assume low-single-digit growth or mild decline in that segment over time. For the group, a Bear Case of 7–9% ARR growth and a 22–25% EBITDA margin now seems more appropriate than a more severe “melting ice cube” scenario.

Updated valuation - no entry here

The conclusion is fairly clear. The old Base Case has moved closer to the old Bull Case. Pexip is now showing better growth, better margins, and a more resilient segment mix than expected. The share price has also moved, so the opportunity is not as cheap as it was at NOK 57, but the business quality has improved meaningfully.

For the model, I would now assume:

Base Case: 14–16% ARR growth, 28–30% EBITDA margin.

Bull Case: 17–19% ARR growth, 30%+ EBITDA margin.

Bear Case: 7–9% ARR growth, 22–25% EBITDA margin.

Pexip has clearly become a better business after Q1-26. Growth has re-accelerated, Secure & Custom is scaling, Connected Spaces looks healthier than feared, and the company is now firmly operating with a Rule of 40 profile. The old Base Case has moved closer to the old Bull Case.

But the stock has moved as well. At around NOK 80 and roughly 6.8x EV/Sales, the market is already giving Pexip credit for much of the improvement. Under my updated Base Case, the implied five-year investment CAGR is around 11%, below my 20% hurdle rate for a single-stock mid-cap position.

To become a Conviction Buy again, I would need either more evidence that high-teens ARR growth can be sustained, or a better entry point. For now, Pexip is a higher-quality company than before, but not yet an attractive enough stock at the current price.