Hexatronic Q1-26: The inflection point is here

Hexatronic reported its Q1 results on April 29, 2026, and the market is finally validating the turnaround. The adjusted EBITA margin has officially turned the corner, climbing to 8.6%.

In Q4-2025, Hexatronic looked like a fallen angel that had finally stopped falling. Q1-2026 suggests something more important: the company may now be entering its next earnings cycle.

The stock is also up 80% since my original BUY recommendation back in December 2025.

In the Q4 write-up I noted the following: The stock price recovery we have seen lately is justified by this de-risking. The “floor” is solid. However, for the stock to truly “fly” back to its former highs, we need to see the margin leverage kick in during the second half of 2026. We need the US fiber volumes to return and the cost cuts to drop to the bottom line.

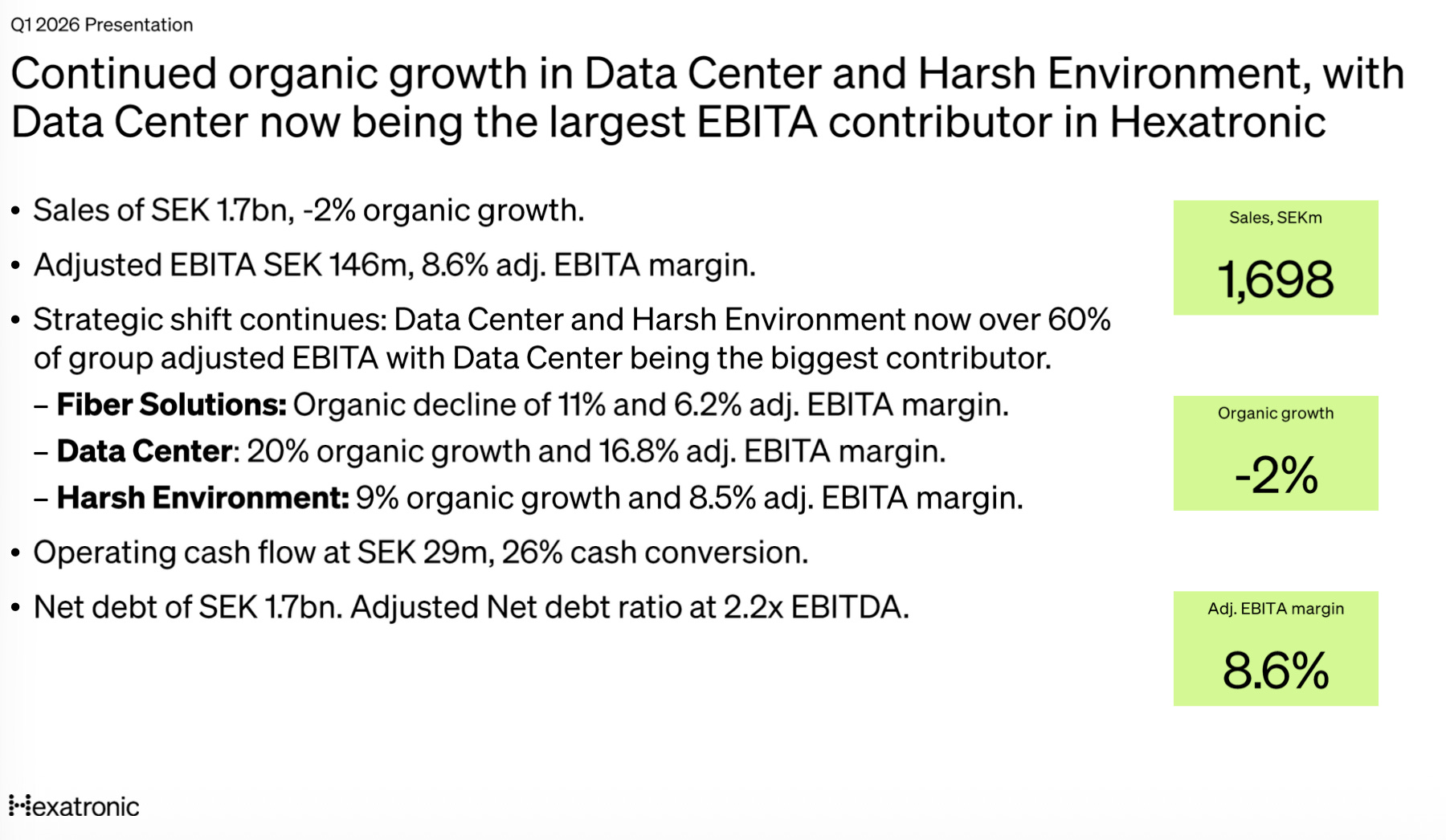

We are starting to see exactly this. After five consecutive quarters of margin compression, adjusted EBITA margin improved sequentially from 7.2% in Q4 to 8.6% in Q1. More importantly, the profit mix has changed. Data Center is now the largest contributor to Group adjusted EBITA, generating SEK 73m in the quarter and overtaking Fiber Solutions.

That matters because Hexatronic is becoming less dependent on the cyclical fiber-utility market and more exposed to structural growth in AI infrastructure, defense, energy, and harsh-environment connectivity. The recovery is still early, especially in Europe, but Q1 provides the clearest evidence yet that the investment case is shifting from “restructuring and survival” to “margin recovery and growth 2.0.”

The Profit Pivot: Data Centers now generate more profit than Fiber Solutions. It should justify a multiple re-rating.

The US Green Shoots: Organic growth has finally returned to the US fiber market, and the “Great Recovery” might be ahead of schedule.

The Margin Bridge: With the SEK 120m cost-savings program now fully implemented, we might see double-digit margins in H2

Offensive Capital Allocation: The JOWO acquisition in Germany signals that management is back on the hunt.

When I wrote in February, the stock was hovering around 28 SEK. Following the Q1 report rally, it now trades around 38 SEK. Some of the easy turnaround money has clearly been made, but the bigger question remains: is the market still valuing Hexatronic as a cyclical fiber supplier, rather than as a broader critical-infrastructure platform?

Q1 beyond the headlines: The 8.6% margin signal

The headline numbers in Hexatronic’s Q1 report were not spectacular at first glance. Group sales declined 10% year over year to SEK 1,698 million, with organic growth at -2%. FX was a major drag, accounting for 9 percentage points of the reported decline, while acquisitions added 2 percentage points. Adjusted EBITA came in at SEK 146 million, down from SEK 184 million a year ago, corresponding to an adjusted EBITA margin of 8.6% versus 9.8% in Q1 2025.

But the more important signal is not the year-on-year decline. It is the sequential improvement. The adjusted EBITA margin rose from 7.2% in Q4 2025 to 8.6% in Q1 2026, ending a five-quarter margin decline. That matters because it suggests the performance improvement program is no longer just a management promise but starting to show up in the P&L. Hexatronic also finalized the initial program during the quarter, with Fiber Solutions seeing a clear sequential margin improvement despite lower sales.

The quarter therefore looks like a transition point rather than a simple weak top-line print. Fiber Solutions is still under pressure, especially in Europe, but margins are stabilizing. Data Center is now the group’s largest adjusted EBITA contributor. Harsh Environment continues to grow organically, even though near-term mix effects temporarily weighed on profitability. In other words, the quality of earnings is increasingly shifting away from legacy FTTH cyclicality and toward more structurally attractive end-markets.

The Tale of Three Segments

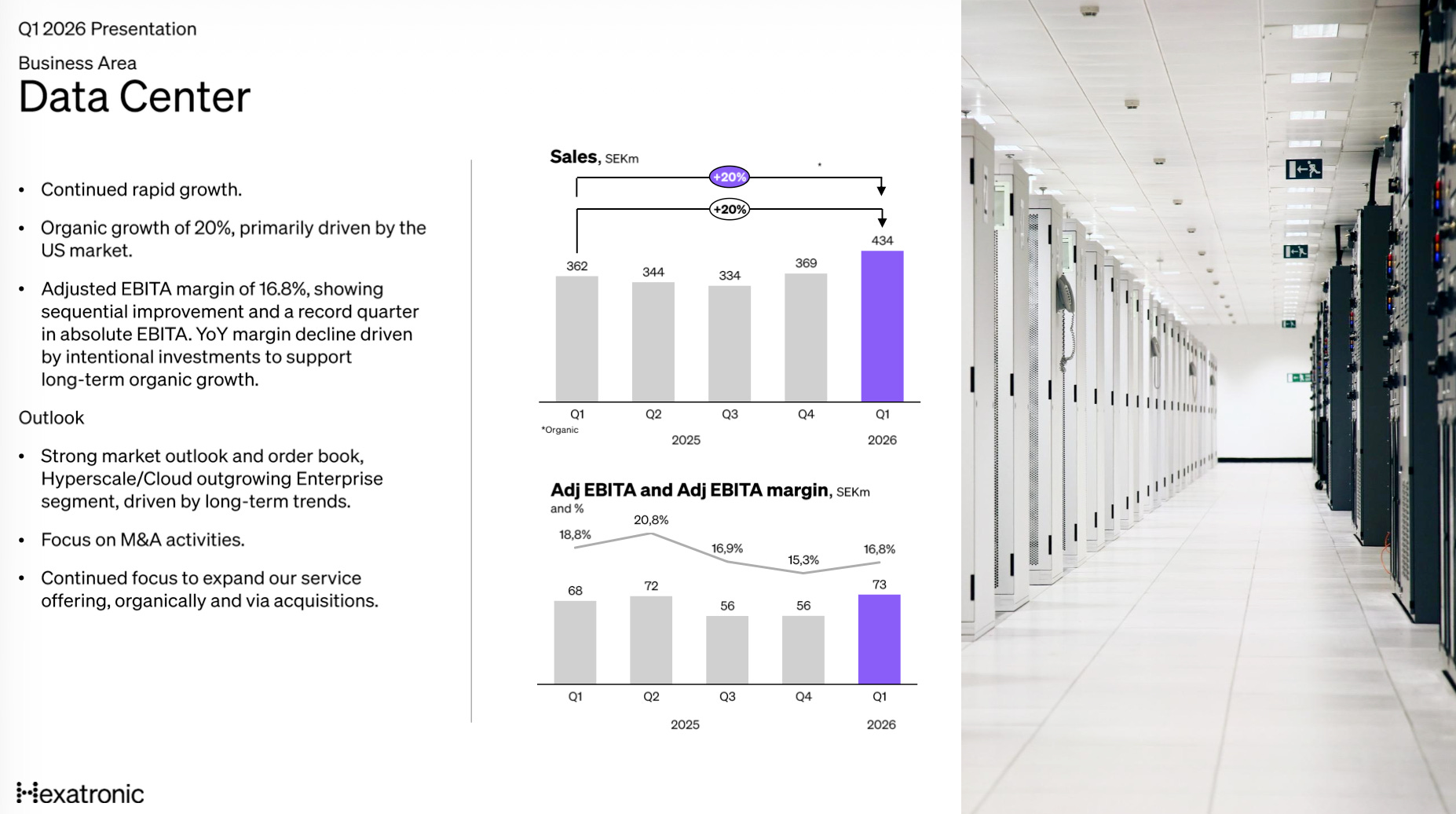

Data Center: The MVP

Data Center was the clear standout in Q1. Sales increased 20% year over year to SEK 434 million, with organic growth also at 20%. Adjusted EBITA reached SEK 73 million, making Data Center the largest contributor to group adjusted EBITA in absolute terms. The adjusted EBITA margin was 16.8%, down from 18.8% a year ago but up sequentially from Q4’s 15.3%.

The key point is that the margin decline is not a demand problem. Management attributes the lower year-on-year margin mainly to deliberate investments in organic growth initiatives and organizational strengthening. In other words, Data Center is absorbing growth investments while still delivering a margin above Hexatronic’s long-term target level for the segment. The company is broadening the offering, including toward campus environments, and that management sees no slowdown in order activity.

This makes Data Center the most important proof point in the quarter. The AI and cloud infrastructure tailwind is no longer a narrative benefit sitting outside the numbers but visible in revenue growth, EBITA contribution, and group mix. The segment accounted for 25% of group sales but 46% of group adjusted EBITA before eliminations, up from 19% and 34%, respectively, in Q1 2025.

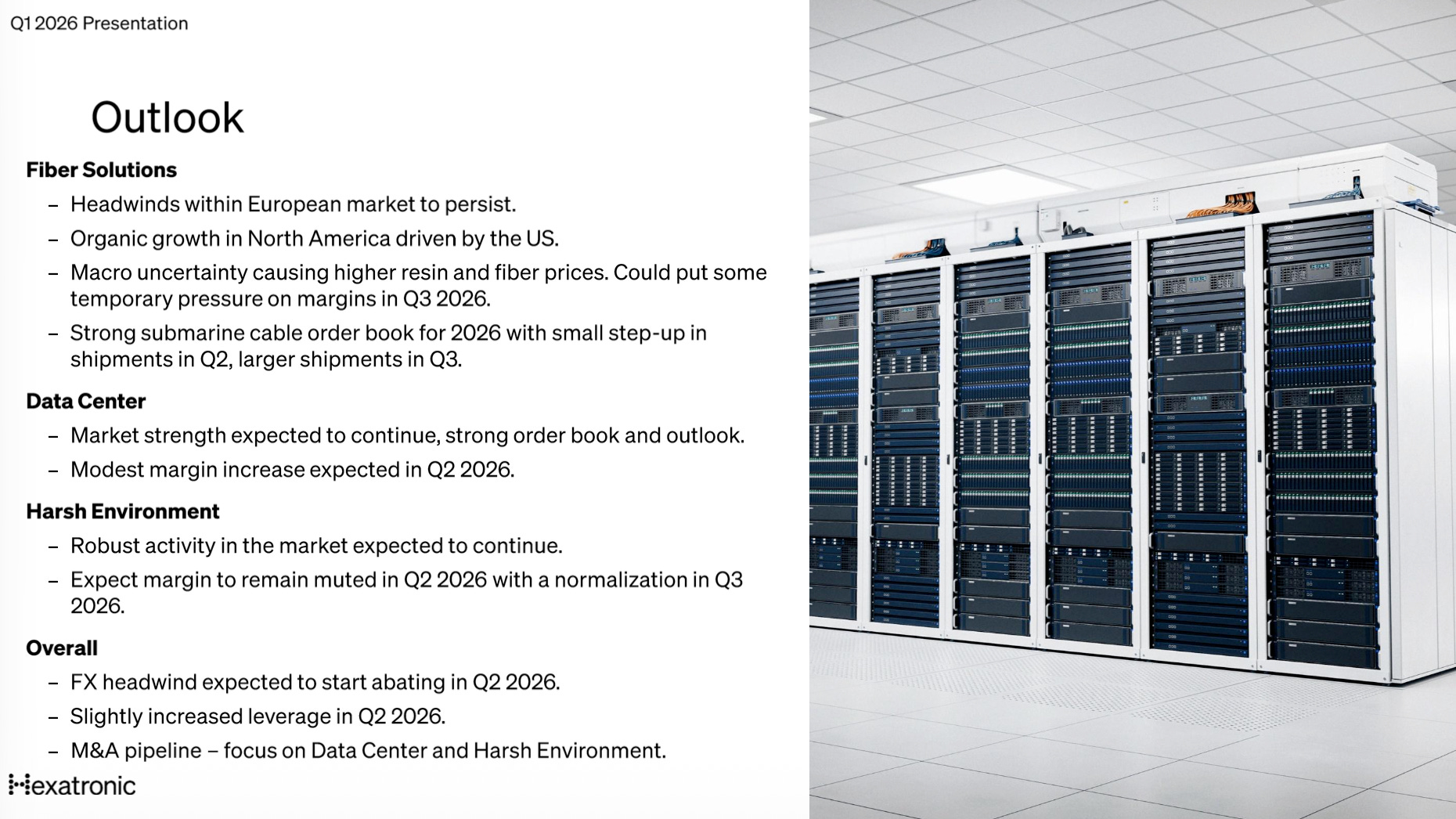

The implication is straightforward. As Data Center becomes a larger part of Hexatronic, the group’s earnings profile should become less dependent on the timing and cyclicality of FTTH investment. The segment is growing at attractive profitability, with management guiding for continued strong demand and modest margin improvement in Q2.

Fiber Solutions: The Stabilizer

Fiber Solutions remains the weak point in the portfolio, but Q1 contained the first credible signs of stabilization. Sales fell 20% year over year to SEK 982 million, with organic growth at -11%. Europe remained the main drag, with weak FTTH demand made worse by an unusually cold winter. The segment also faced price pressure and lower capacity utilization.

However, the quarter was not purely negative. The US fiber business returned to positive organic growth, a major milestone after a prolonged downturn. This improvement came earlier than expected and was consistent with management’s recovery guidance for 2026. Management also expects positive organic growth in the US to continue into Q2.

The more important detail is margin resilience. Despite the sales decline, Fiber Solutions delivered adjusted EBITA of SEK 61 million and a 6.2% margin, up from 5.2% in Q4 2025. The restructuring program appears to be the main driver, with cost savings realized slightly ahead of the original plan. That matters because Fiber Solutions is still Hexatronic’s largest sales segment, representing 58% of group sales in Q1, so even modest margin stabilization has a meaningful group-level impact.

The outlook is mixed but improving at the edges. Europe is expected to remain challenging as the FTTH market shifts from building “homes passed” toward connecting subscribers. At the same time, North America is validating management’s expected recovery path, and submarine cable demand remains strong, with a fuller order book for 2026 and larger shipments expected in Q3.

The investment case for Fiber Solutions is therefore no longer about near-term growth. It is about downside control. If Europe stays weak but stops deteriorating, the US continues to recover, and restructuring savings hold, the segment can become a stabilizer rather than a drag.

Harsh Environment: The Sleeper

Harsh Environment delivered the most interesting revenue surprise. Sales came in at SEK 283 million, broadly flat year over year on a reported basis but up 9% organically. Growth was driven by both dynamic cables and connectivity solutions, confirming that demand remains healthy across the segment’s key end-markets.

Profitability was the weaker part of the story. Adjusted EBITA was SEK 24 million, corresponding to an 8.5% margin, down from 10.3% a year ago. The decline was driven by an unfavorable product mix and timing effects, including lingering effects from the 2025 US government shutdown. Management expects some additional margin pressure in Q2 before a normalization in Q3.

That said, the strategic direction remains attractive. The segment is exposed to defense, energy, offshore, marine technology, aerospace, and other demanding environments where connectivity reliability is mission-critical. These are not low-quality cyclical end-markets. They are areas where technical requirements, customer relationships, and specialized products can support more resilient long-term demand.

The announced acquisition of JOWO Systemtechnik strengthens this story. JOWO is a German manufacturer and distributor of connectors and related products serving primarily defense, energy, and industrial customers. The acquisition expands Hexatronic’s connectivity solutions exposure and gives Harsh Environment a broader platform in Europe.

For now, Harsh Environment is a “sleeper” because the near-term margin print does not fully reflect the segment’s longer-term potential. The demand signals are solid, the order activity remains robust, and management continues to prioritize M&A in connectivity solutions. If margins normalize after Q2, Harsh Environment could become a larger and more strategically important earnings contributor.

Checking the pulse on the US

The “US Recovery” thesis is being validated in real-time by the hard data. Management confirmed that conditions in North America have shifted from stabilization to “gradual improvement,” explicitly guiding for continued positive organic growth in Q2 2026. This is a massive milestone. Q1 marked the first time the US fiber business returned to positive organic territory in over a year, signaling that the industry-wide inventory correction has finally washed through the system.

While commercial demand is providing the current lift, the massive Broadband Equity, Access, and Deployment (BEAD) program is finally moving to implementation. As of early May 2026, 54 states and territories had received NTIA approval for their final BEAD proposals, while 52 had NIST approval making grant funds available and 50 had signed award agreements.

The 2025 restructuring moved BEAD toward a more technology-neutral framework and, according to NTIA, delivered an estimated $21bn in savings. Large US operators are already preparing for a heavier 2026 deployment cycle, but the exact timing and technology mix of BEAD-driven demand remains uncertain.

Hexatronic management continues to timestamp the primary BEAD momentum for H2 2026, but the fact that the US market is growing ahead of this stimulus is the real bull case. We are looking at a “double-wave” recovery: commercial demand is rebounding now, just as the largest federal investment in broadband history enters its four-year execution window starting this summer.

And what about M&A?

With the balance sheet stabilized and leverage well within the targeted range, offensive M&A is officially back on the table. The headline move this quarter was the acquisition of JOWO Systemtechnik AG, a specialized German player in high-performance connectivity solutions. This is a strategic expansion into the European defense, aerospace, and energy sectors, which are currently seeing unprecedented structural investment. JOWO brings a prestigious tier-1 customer base and a stellar financial profile, generating approximately EUR 13 million in annual sales with an exceptionally high EBITA margin of ~20%.

This acquisition is the final piece of the puzzle for the Harsh Environment business area, which now reaches a critical mass of SEK 1.5 billion in pro forma annual net sales. By folding JOWO into the Group, Hexatronic has successfully built a high-margin, non-cyclical pillar that provides a powerful hedge against the volatility of the fiber market. Management noted that the M&A pipeline remains active, with a clear focus on “critical digital infrastructure” businesses that offer the same blend of technical complexity and recurring defensive demand.

Update on the performance improvement program

The initial phase of the performance improvement program, first announced in Q3 2025, was officially finalized this quarter, with management realizing the majority of the projected cost savings slightly ahead of the original schedule. These efficiencies were the primary engine behind the sequential recovery in the Adjusted EBITA margin, which climbed to 8.6% (up from 7.2% in Q4).

While the 26% cash conversion (SEK 29 million operating cash flow) appears lower on paper, it was heavily influenced by a sharp spike in accounts receivable following an exceptionally strong end to March. Despite a slight uptick in adjusted leverage to 2.2x (due to currency headwinds and a tough comparison against a record Q4 EBITDA) the balance sheet remains robust with SEK 603 million in liquid assets.

Is the “Fallen Angel” flying? Valuation update

Hexatronic is entering the summer with:

A repaired margin profile that is expanding sequentially.

A “rather full” order book for submarine cables for the rest of 2026.

A structural mix shift toward high-margin Data Center and Defense revenue.

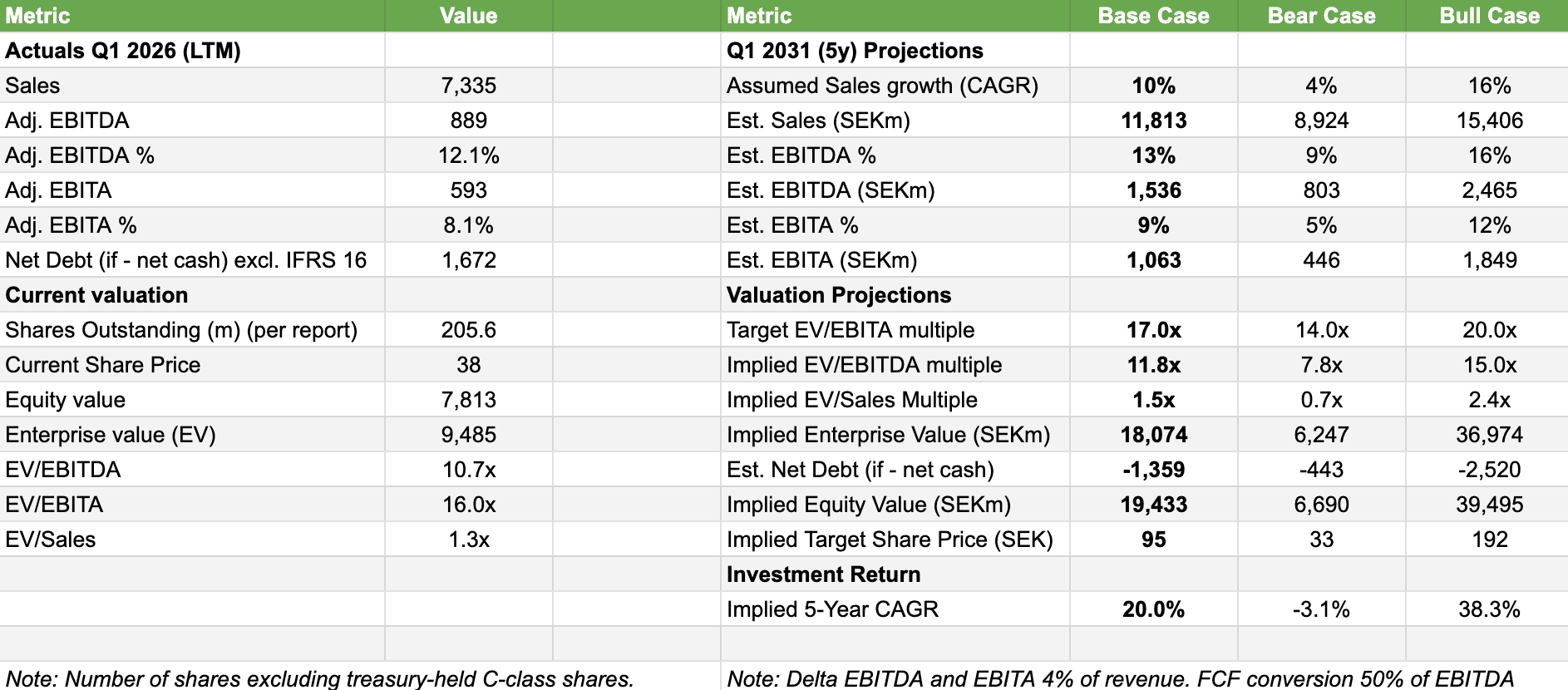

When plugging the numbers into my valuation model, it remains a BUY for me, although the margin of safety has narrowed. My base case assumes 10% sales CAGR, a 9% EBITA margin, 50% EBITDA-to-FCF conversion, and a 17x EV/EBITA exit multiple. That produces a 2031 target price of roughly SEK 95 per share, implying around 20% annualized return from today’s level. The key sensitivity is the exit multiple: this target assumes the market increasingly values Hexatronic as a diversified critical-infrastructure platform rather than a purely cyclical fiber supplier.

My Verdict: Q1 was an inflection point. I am maintaining my BUY rating as we move into the seasonally stronger H2, where the full impact of cost cuts and US growth may drive significant earnings beats.

Over and out.

Congratulations. Very well written. I actually read your first report and was very close to pulling the trigger - actually I had a buy order that never got filled as it moved too quickly. Kicking my ass for not just buying at 24 SEK and hoping for the drop to 22 SEK.

In terms of valuation - agree - the easy gains have been made. I would say the stock price is close to moving ahead of operational developments...